What is a virtual account?

A virtual account is a digital sub-account, with its own bank ID, associated with a physical bank account.

Virtual accounts make it easier to track and matching incoming and outgoing cash flows: incoming and outgoing funds are allocated directly at source (by customer, subsidiary, supplier, activity, etc.), without the need to create a separate physical bank account for each use.

What is an In-House Bank ?

An In-House Bank (IHB) is a group-internal financial entity whose mission is to centralize all or part of the Group’s treasury and financing functions. It acts as an internal bank for its subsidiaries, offering services such as internal financing, risk management (FX, IR, etc.) and payments.

The IHB can therefore make payments and grant financing to its subsidiaries according to pre-defined conditions that can be parameterized in its TMS. Subsidiaries can use a dedicated portal, such as Datalog TMS, to initiate financing requests, or the group treasurer can use the Payment Factory to make payments and/or collections on their behalf.

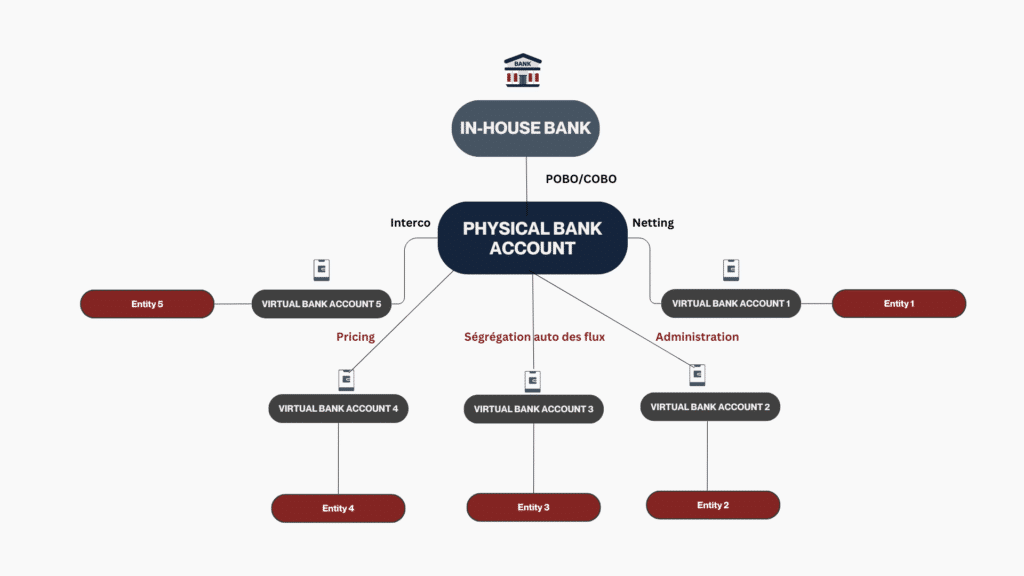

The role of Virtual Accounts in the In-House Bank (IHB)

The ability of virtual accounts to organize and finely segment flows within a single physical bank account makes them a key lever for the In-House Bank.

In practical terms, these virtual accounts act as internal registers, reflecting at each credit or debit the receivables and payables between the IHB and its various subsidiaries. In this way, the IHB can directly assign all intra-group operations such as payments, receipts and interco transactions to the virtual accounts of the corresponding subsidiaries, while maintaining the group’s flows in a single physical bank account.

Thanks to this system, the Treasurer, as the pilot of this internal bank, streamlines his processes, benefits from improved visibility, optimizes bank reconciliation while reducing costs.